Solutions/Underwriting & Modeling

Every underwriting desk, one platform

Personal lines, commercial lines, portfolio and product, CAT and actuarial, all need property data — each at a different scale and with different questions. NE Provenance serves the full underwriting and analytics operation from a single platform, with data available as parquet files, API access, per-property wallets, and other formats your data and UW teams already work with today.

From individual submission decisions to territory-level portfolio management to parcel-level catastrophe exposure — the same intelligence foundation powers every underwriting workflow.

Jump to your workflow

Personal Lines

Property-level data for every submission

Commercial Lines

Business classification meets property data

Portfolio / Territory

Territory-level data at parcel resolution

Product Underwriting

Define segments that weren't possible before

CAT / Hazard

Parcel-level catastrophe exposure — not ZIP-level guesses

Actuarial & Modeling

Property-level variables for loss cost and rate modeling

Personal Lines

Property-level data for every submission

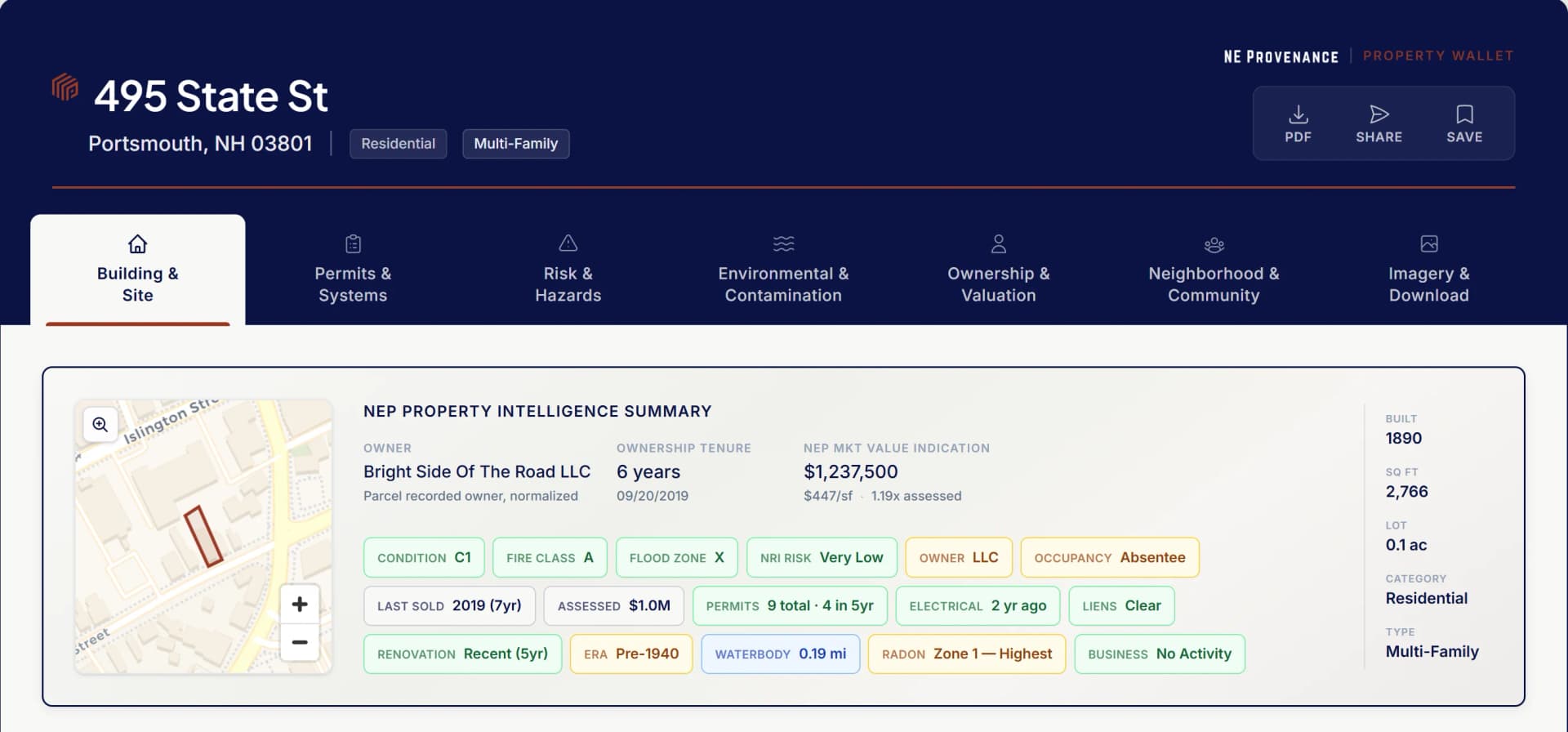

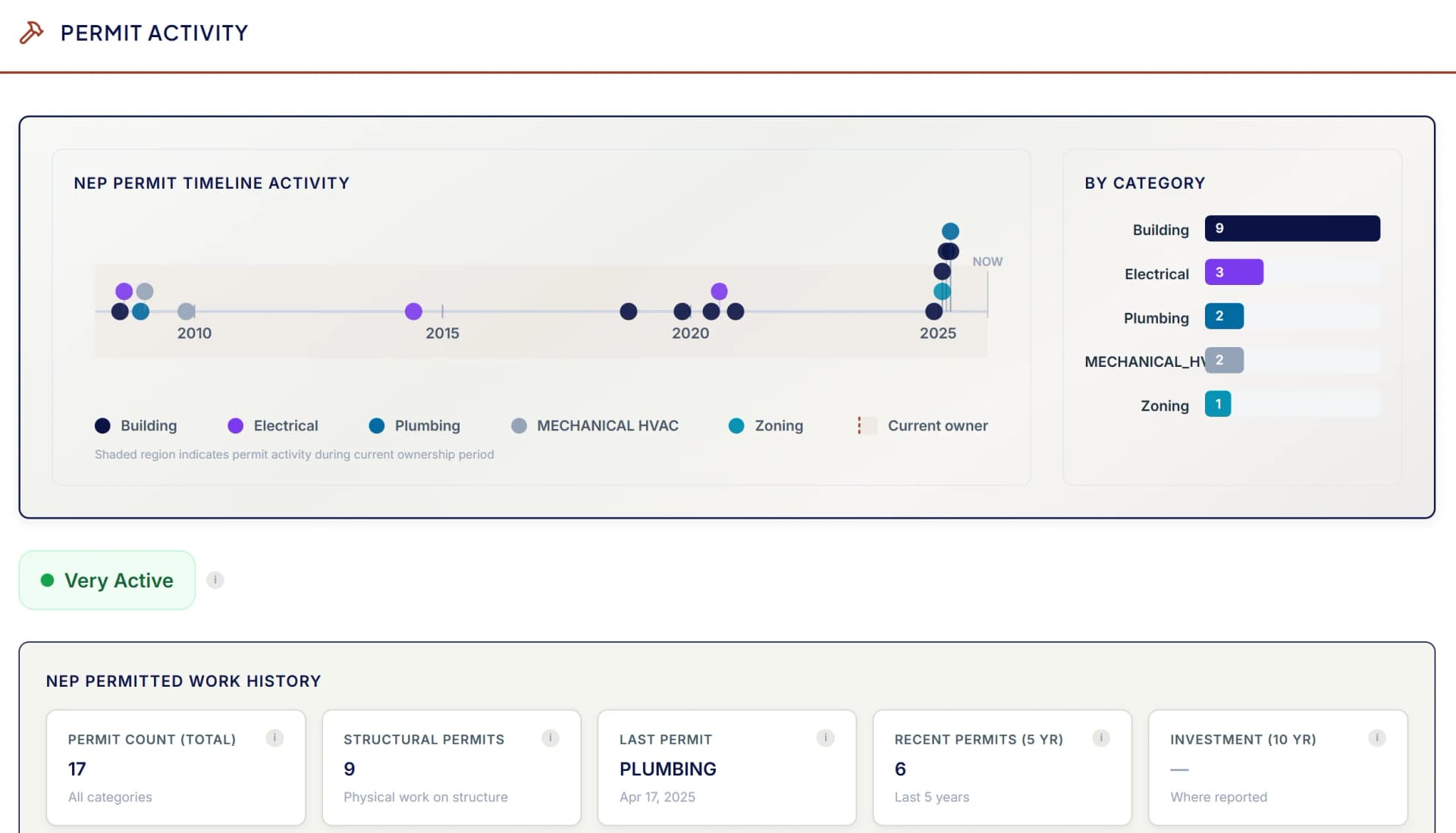

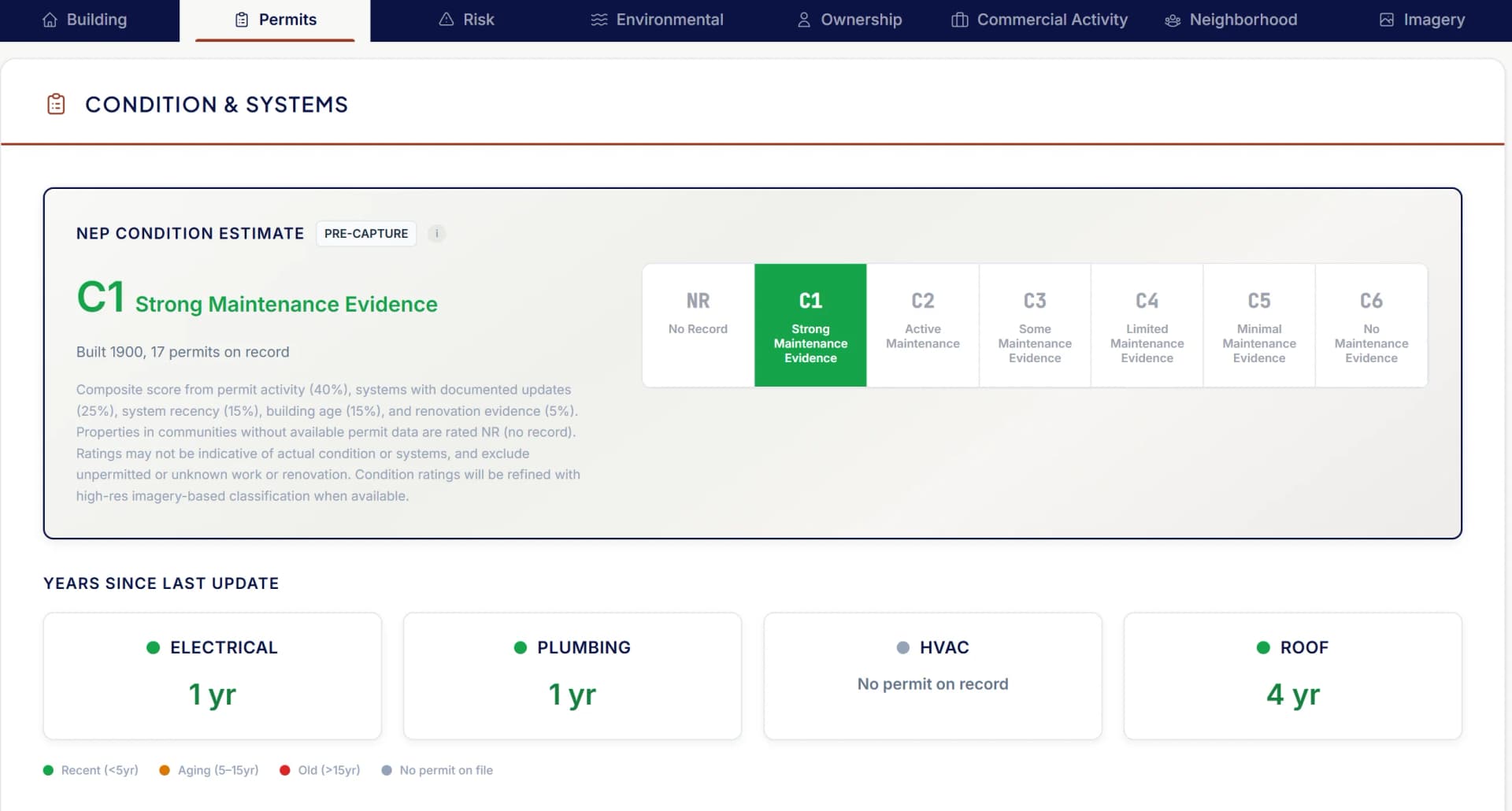

A PL underwriter evaluates individual properties — accept, reject, modify. The Property Wallet delivers instant property data from 140+ sources — building characteristics, condition rating, environmental exposure, ownership data, risk indicators, and where available, permit history and systems age — giving underwriters a comprehensive view before any field activity.

An underwriter in Boston receives a submission for a 1924 colonial in Portsmouth, NH. Before ordering an inspection, they pull the Property Wallet: C3 condition estimate, 2 permits in five years (electrical 2022, plumbing 2020), flood zone X, owner-occupied, fire protection grade B. Submission triaged in minutes with evidence on file.

What you get

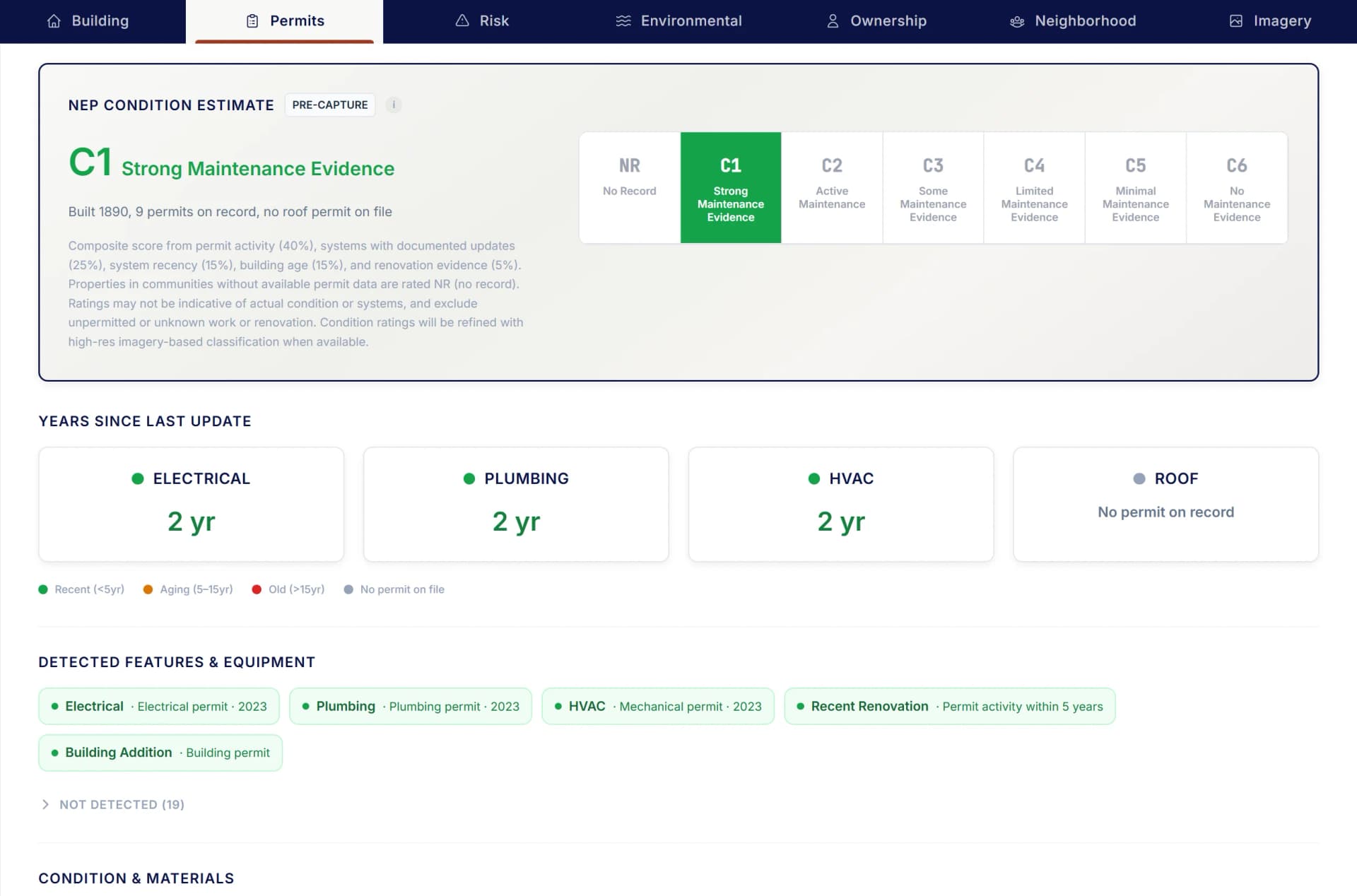

- Condition estimate (C1–C6) derived from permit activity, building age, and ownership signals

- Building characteristics, year built, style, stories, lot size

- Permit-derived systems age: electrical, plumbing, HVAC last permitted dates

- Risk indicators: fire protection grade, environmental exposure, ownership patterns

- Fire protection grade (A–E): station distance + municipal water/sewer service

- Environmental exposure: flood, surge, wind, contamination

- Aerial imagery of the parcel and lot layout from state-level imagery programs

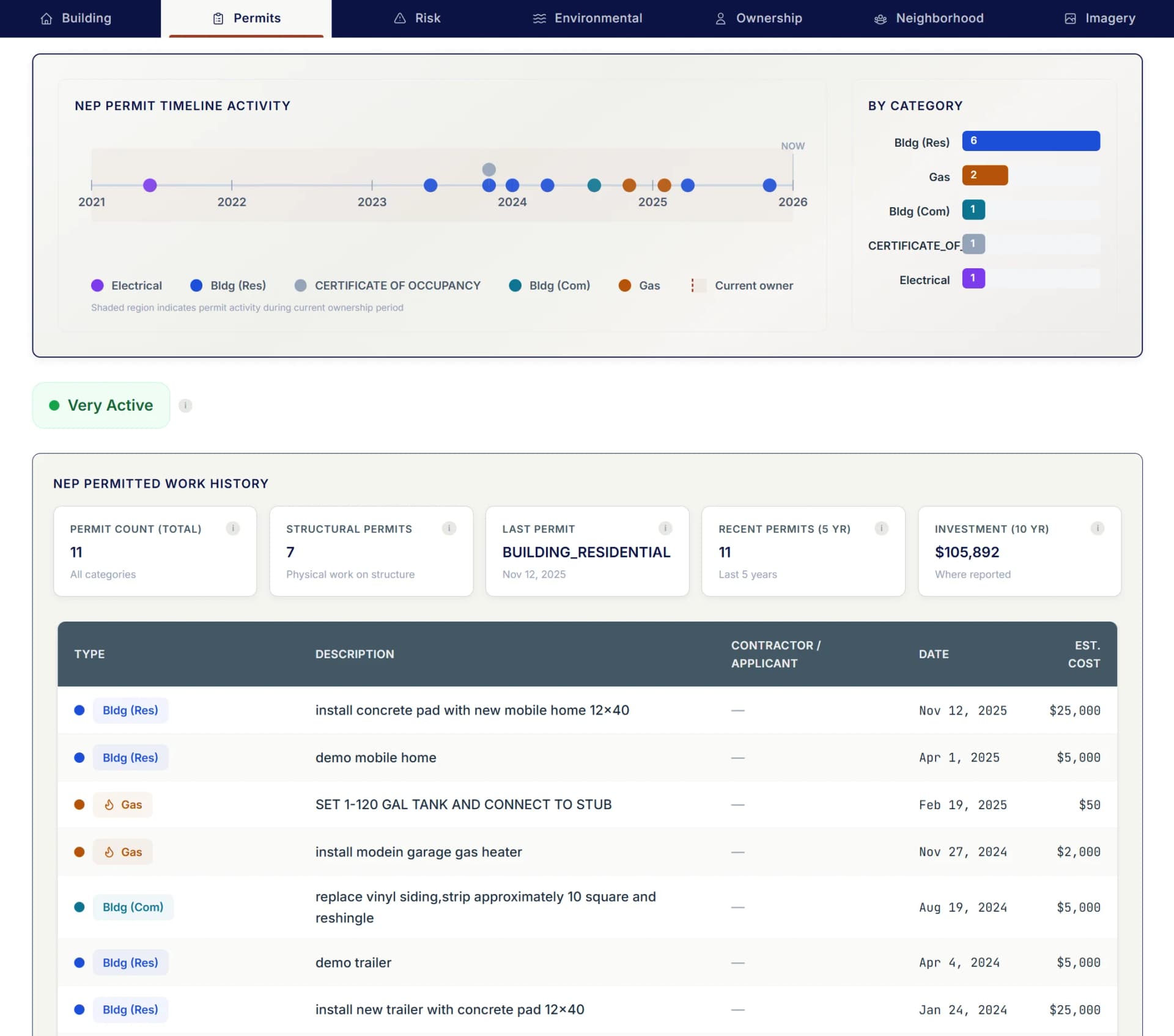

Commercial Lines

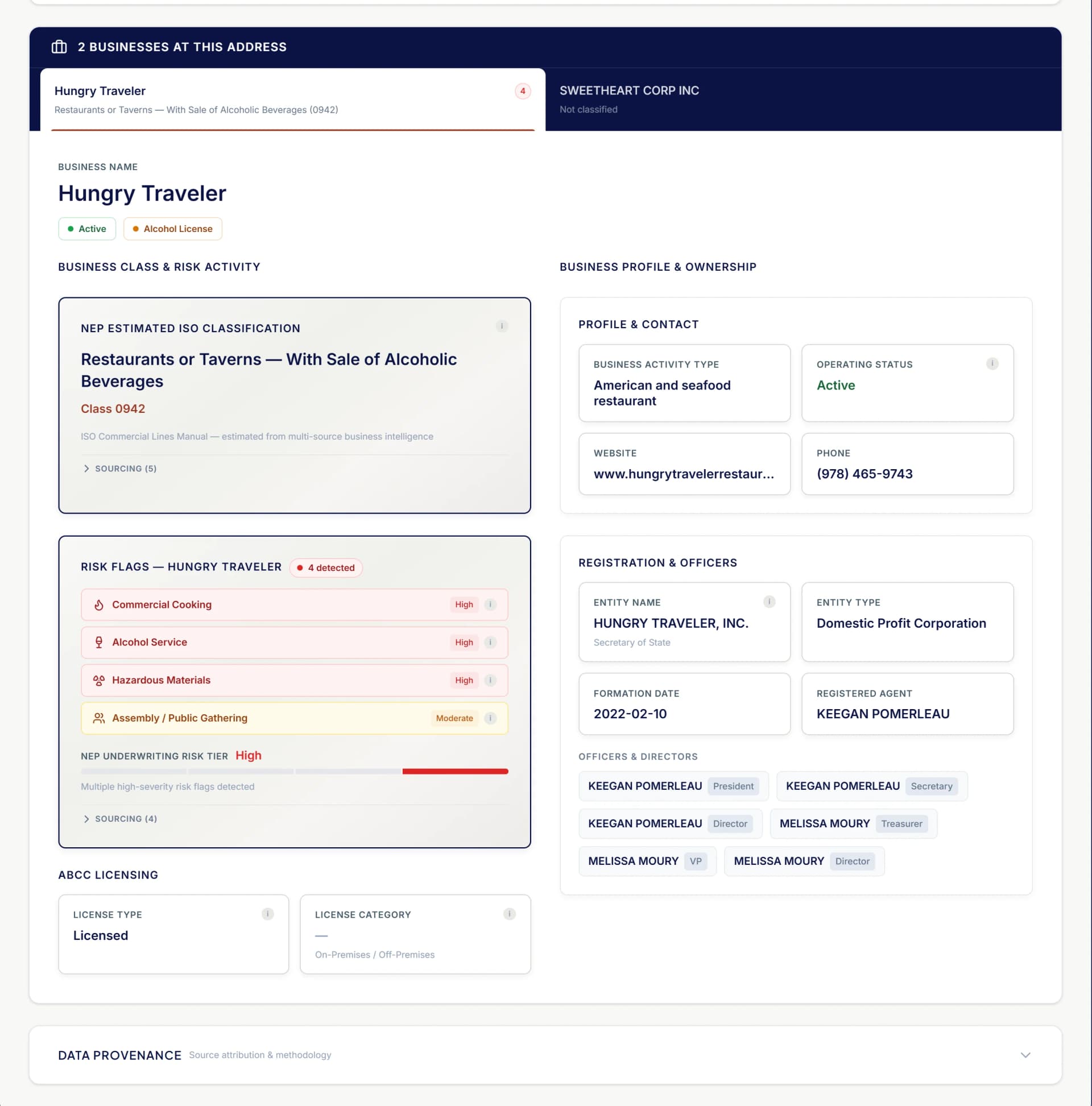

Business classification meets property data

Commercial underwriting needs everything PL needs plus a critical layer: what business operates here, what are the operational hazards, and how should it be classified? NE Provenance triangulates business intelligence from multiple sources to answer these questions.

A commercial lines underwriter is reviewing a submission for a mixed-use building in downtown New Haven, CT. The Property Wallet shows: ground-floor restaurant (state liquor license confirmed), two residential units above, commercial cooking confirmed via Foursquare business data, no fire suppression permit on file, last building permit 2024. The NEP Estimated ISO classification is pre-populated. The hazard profile is clear before the underwriter picks up the phone.

What you get

- Business name and type from signage, Foursquare, Google Places, Secretary of State

- ISO/BOP commercial class code assignment

- Alcohol service: ABCC license cross-reference

- Cooking operations: identified from business classification, licensing data, and AI extraction

- Hazmat indicators: EPA underground storage tanks, MassDEP releases, business classification

- Mixed-use identification and occupancy breakdown

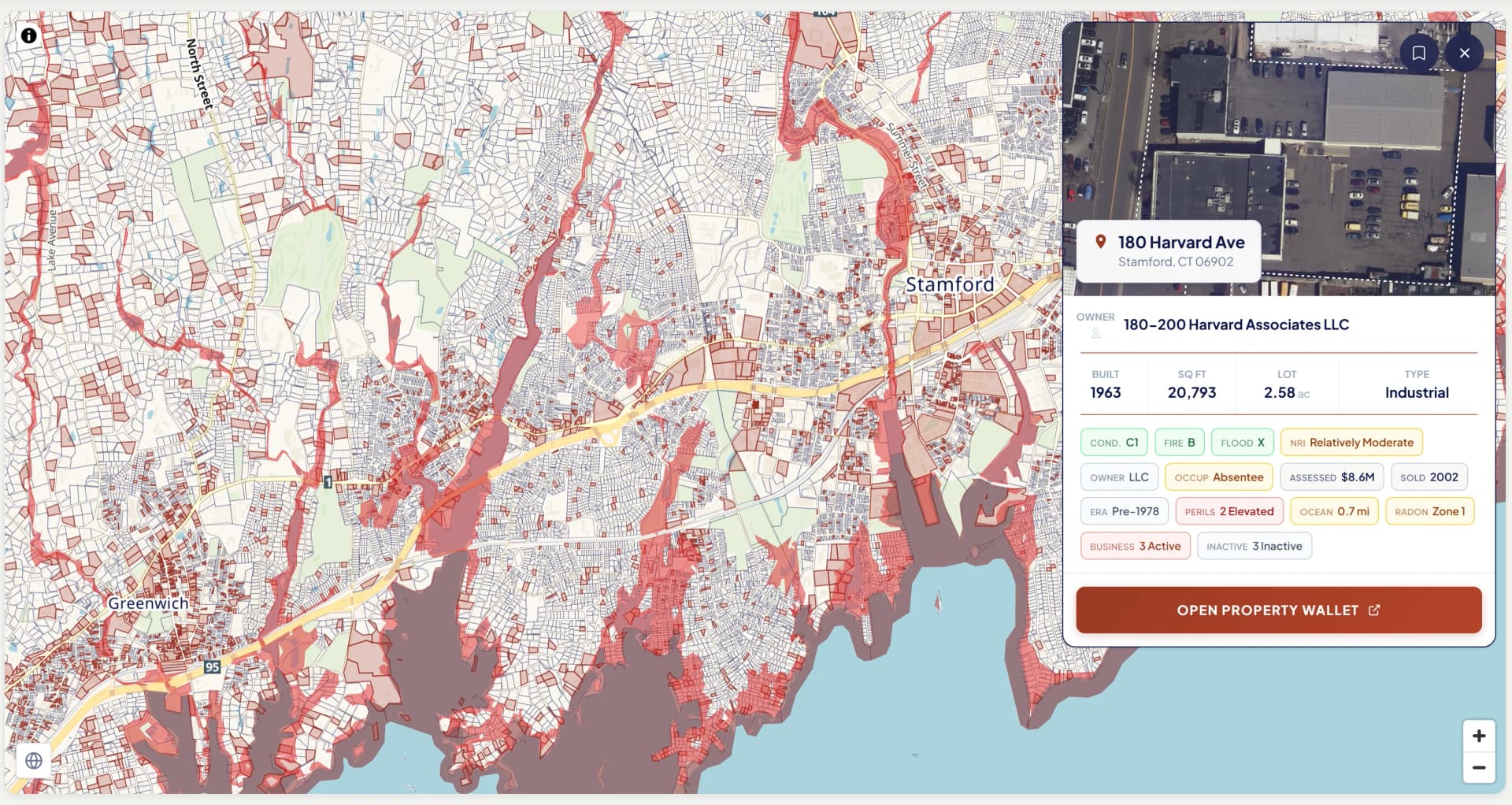

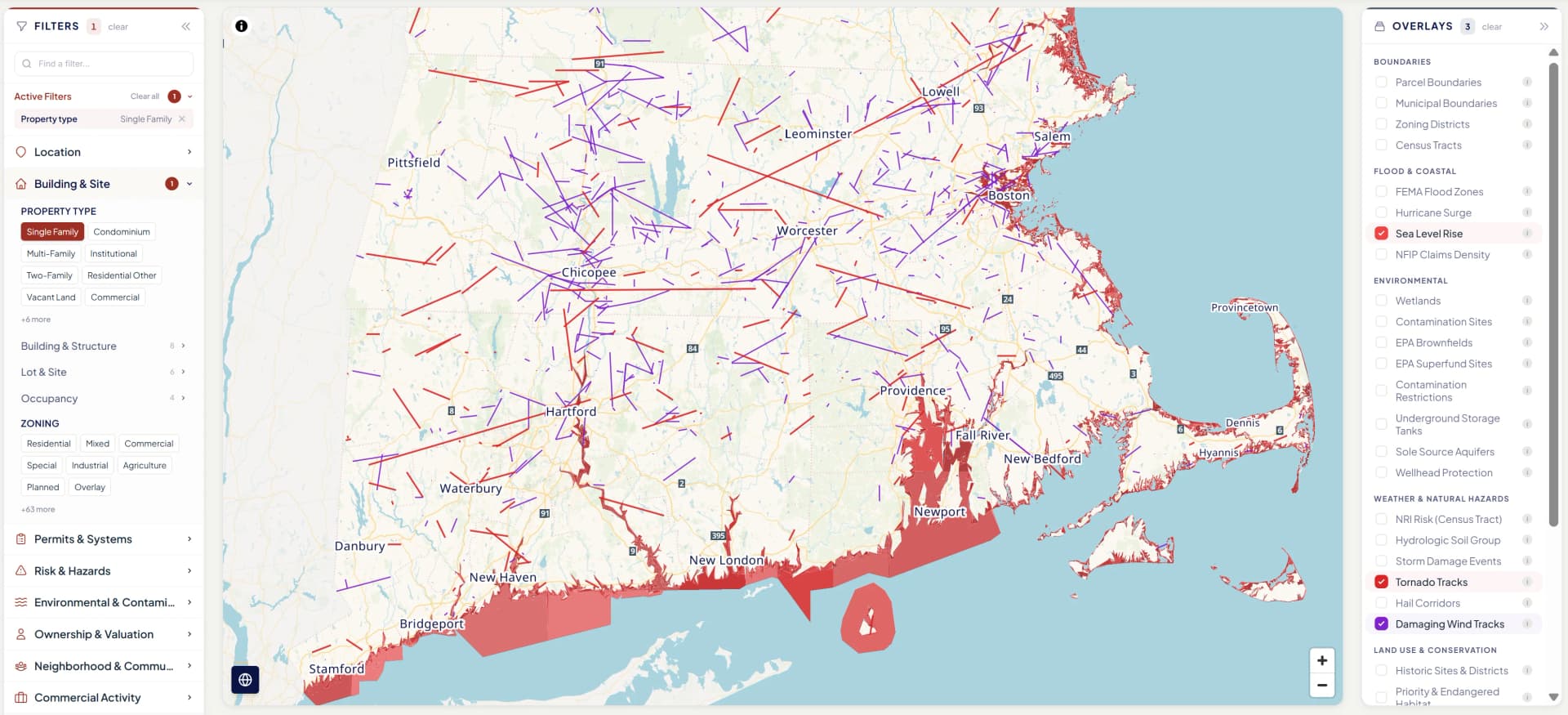

Portfolio / Territory

Territory-level data at parcel resolution

Portfolio underwriters manage territories, not individual properties. They need to answer "should we write more or less here?" NE Provenance gives them condition distributions, risk concentrations, and age cohort analysis across thousands of properties — the kind of data that was never available for New England at this scale.

A territory manager is preparing for a quarterly portfolio review of their coastal Massachusetts and Rhode Island book. They import 8,500 policy addresses into NE Provenance. The map instantly shows risk concentrations: 680 properties in AE flood zones, 173 with prior NFIP claims, 2,400 with no building permit in 10+ years. They filter to "wood frame, coastal, C4 or worse" and export a 94-property watch list for field review.

What you get

- Condition distributions across any geography — town, county, ZIP, custom territory

- Age cohort analysis: building vintage, construction era, systems age from permits

- Permit activity rates: renovation velocity by area

- Environmental exposure concentrations: flood, surge, wind by territory

- Risk flag aggregations: permit-gap cohorts, absentee ownership, environmental exposure, fire protection gaps

- Ownership patterns: absentee rates, LLC concentrations, portfolio owners

Product Underwriting

Define segments that weren't possible before

Product underwriters analyze which products and coverages are profitable in which segments. The challenge has always been that you can't define meaningful segments without property-level attributes. NE Provenance gives you the attribute depth to build segments like "coastal wood-frame properties with no roof permit and absentee owners" — and actually quantify them.

A product analyst is investigating why wind claims across coastal New England are 40% above expectation. They query NE Provenance: of the 28,000 coastal properties in their book, 7,200 are wood frame with no building permit in 10+ years and C4 or worse condition ratings. That segment — identifiable only with this data — accounts for 72% of the excess loss. A targeted underwriting action on 7,200 properties addresses the portfolio problem.

What you get

- Slice portfolios by construction type, condition, age, territory, owner type

- Cross-reference property attributes with your own loss experience data

- Identify micro-segments driving disproportionate loss costs

- Quantify the book impact of underwriting actions before implementation

- Track segment composition changes over time as properties age and change

- Export segment definitions for integration with pricing and analytics systems

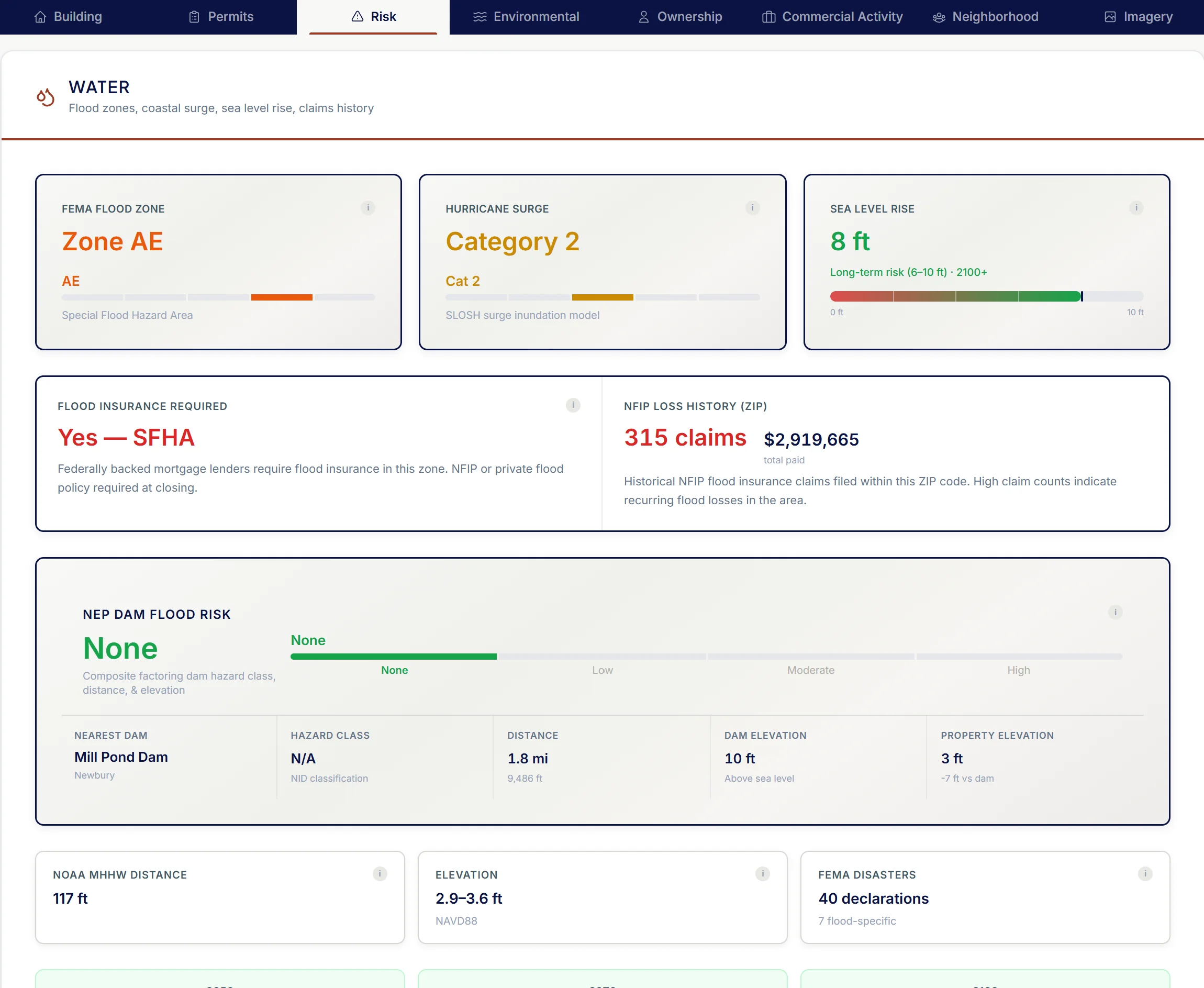

CAT / Hazard

Parcel-level catastrophe exposure — not ZIP-level guesses

CAT underwriting has historically been stuck at ZIP or census tract aggregates because parcel-level data didn't exist at scale. NE Provenance changes this. Every property has precise flood zone, surge zone, sea level rise exposure, wind design speed, soil data, and wildfire risk — layered with building characteristics and condition estimates that determines vulnerability.

A CAT modeler is evaluating coastal wind exposure for portfolio accumulation analysis. They query: "all properties within 1 mile of the coast, wood frame, in surge zones Cat 1–3." The result: 8,400 properties with precise building characteristics, condition rating, elevation, and fire protection grade. The modeling team can quantify probable maximum loss with property-level granularity instead of ZIP-level assumptions. Mid-tier carriers especially benefit — this is RMS/AIR-grade exposure data at a fraction of the cost.

What you get

- FEMA flood zones at the parcel level — AE, VE, X, with BFE where available

- Hurricane surge zones (SLOSH model) — Cat 1 through Cat 4

- Sea level rise exposure: NOAA projections at 1ft, 3ft, 6ft

- ASCE 7-22 design wind speeds for precise location

- Hail exposure: radar MESH data and SPC historical reports

- Soil data: SSURGO drainage, shrink-swell, foundation risk

Actuarial & Modeling

Property-level variables for loss cost and rate modeling

Actuarial and modeling teams have historically relied on ZIP-level or census tract aggregates because parcel-level property attributes were unavailable at scale. NE Provenance delivers 430+ property-level variables — condition, construction, age, systems, hazard exposure, and ownership — as modeling inputs that replace or supplement aggregate proxies.

An actuarial analyst is building a loss cost model for coastal homeowners. Instead of using ZIP-level age-of-home proxies, they pull NE Provenance data: actual building age, permit-derived roof age, condition rating, flood zone, surge zone, and construction type for 45,000 properties. The model's predictive power improves materially because the inputs are property-specific, not geographic averages.

What you get

- Building age, construction type, and materials at the parcel level — not ZIP proxies

- Permit-derived systems age: when the roof, electrical, plumbing, and HVAC were last updated

- NEP Condition Rating (C1–C6/NR) as a continuous variable for loss cost segmentation

- Parcel-level hazard exposure: flood, surge, wind, hail, wildfire — not aggregated

- Ownership characteristics: entity type, tenure, absentee indicators, portfolio detection

- Bulk Parquet delivery for direct integration into modeling pipelines and data warehouses

The public records substrate

Data that traces to dated, cited sources

Property Wallet attributes are sourced and provenance-tracked. When a permit date appears in the record, the underwriter knows when it was pulled, what jurisdiction issued it, and what scope of work it covered. Pipeline refreshes add newly recorded permits, deeds, and assessor updates as jurisdictions publish them — typically on a monthly cadence, faster for counties with electronic filing. Permit and deed coverage varies by jurisdiction and is expanding.

Building permits

Permits on file for the parcel — date, scope, contractor where listed. Additions, renovations, electrical, plumbing, HVAC, roofing, and demolitions sourced from municipal permit offices across New England. Coverage expanding continuously.

Deed transfers

Recorded deeds with date, price, grantor, grantee, and instrument type sourced from county registries of deeds across New England. Deed coverage varies by county and is expanding.

Entity resolution

LLC, trust, and corporate ownership resolved across parcels. Portfolio detection surfaces the other parcels the same entity controls.

Mortgage and lien recordings

Mortgage terms, lien filings, discharges, and lis pendens sourced from registry of deeds. Mechanic's liens from permit records.

Assessor updates

Annual assessment changes, classification, exemption status, and ownership records from the municipal assessor of record.

Environmental filings

21E/AUL records, UST registrations, wetlands designations, dam hazard classifications, and state environmental agency filings.

Regulatory aligned from day one

Attributes carry data provenance: the source chain showing where data originated and how it reached the property record. As imagery-based underwriting frameworks evolve across New England — Massachusetts Bulletin 2025-02, Rhode Island, and New Hampshire — our provenance infrastructure is designed to satisfy the documentation requirements carriers will face.

This isn't an afterthought. It's designed to satisfy carrier audit requirements and regulatory documentation needs from the start.

COPE

ISO

NEP C1–C6/NR

ACORD

FEMA NFIP

ASTM E2018

Fraction

of the cost of a traditional exterior inspection

Instant

At point of quote via API — no scheduling, no wait

140+

Independent data sources corroborated per property

430+

Attributes per property — via UI, API, batch, or bulk feed

Working together

We understand underwriting operations because we've built them

Whether you need per-submission data at point of quote, portfolio-level enrichment for a book review, or parcel-level exposure data for your modeling team — we'll work with you to get the integration right. That means understanding your existing systems, your data formats, and your decision workflow.

Every conversation starts with Mike directly — 17 years of underwriting operations experience, building the workflows this data is designed to serve.

Explore the intelligence for yourself

Open a Property Wallet for a real New England property. With over 4.7 million similar records across all six New England states, see how it fits into your workflow.

Newburyport, MA · Federalist · 3,524 sq ft · 4 bed / 3 bath · Built 1800 · Historic District

NEP Property Intelligence Summary

ConditionC1Fire ClassBFlood ZoneXOwnerIndividualOccupancyOwner-Occupied

Purchased2018 (8yr)Permits11 total · 4 in 5yrSystems3 updated · newest 0yrLiensClearAssessed$1.6MOcean0.3 miSurgeCat 2

EraPre-1940HistoricDesignatedRenovationRecent (5yr)CommercialNo Business ActivityRadonZone 1 — Highest

AES-256 encryption

US-hosted infrastructure

CCPA compliant

Customer data never sold or shared

Authoritative, primary sources

PostgreSQL — enterprise-grade infra