Solutions/Lending

Collateral data across the loan lifecycle

Lenders need to know the property behind the loan — its condition, its risk profile, its environmental exposure, and its market context. NE Provenance delivers property data that enriches every stage of the lending process, from origination through portfolio review.

The same data that serves your underwriting decisions also feeds your portfolio management — condition trends, ownership changes, and risk signals tracked continuously across your entire book.

Lending workflows

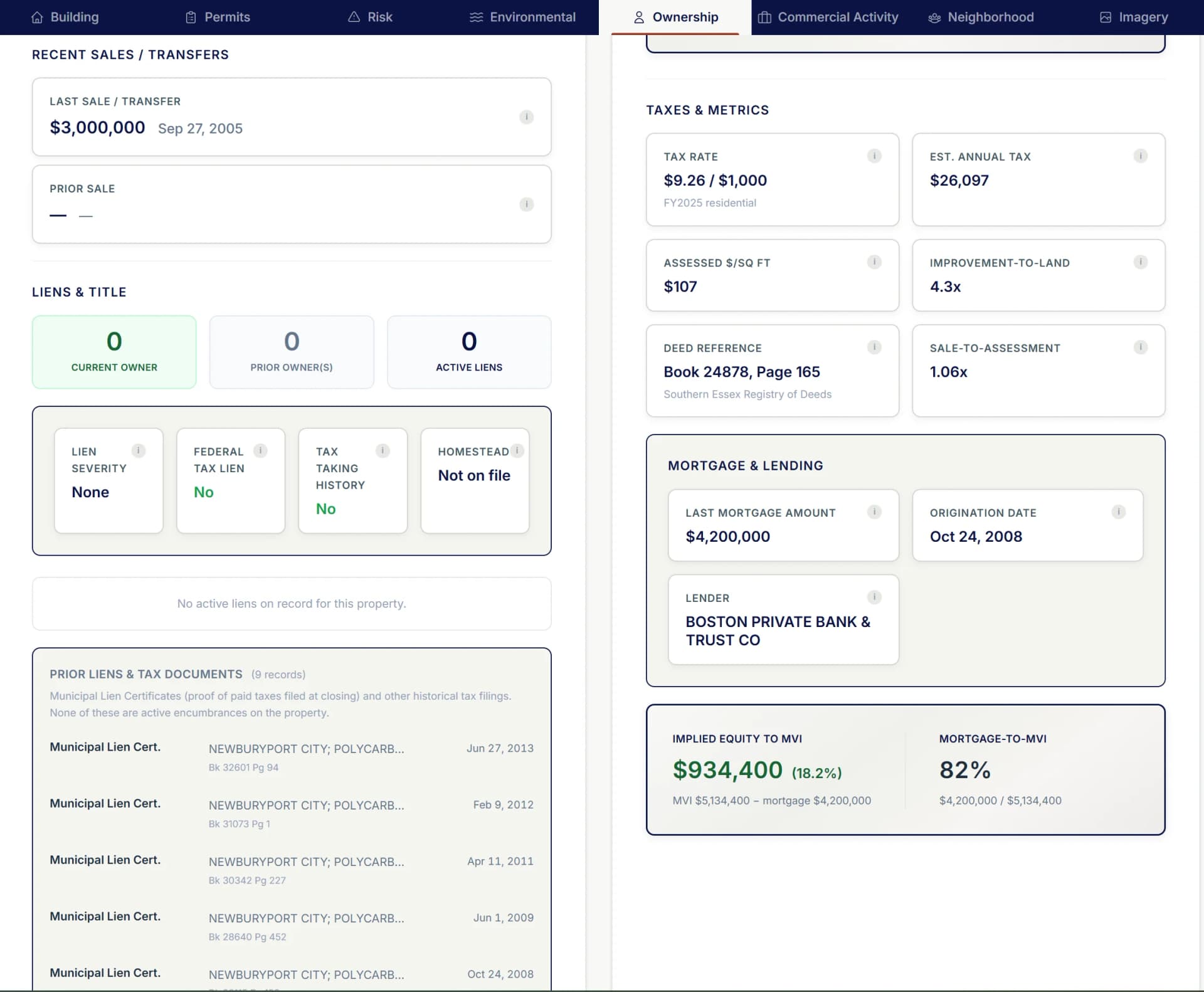

Property data across the lending lifecycle

Origination & Collateral Assessment

Validate collateral quality at the point of origination. Condition estimate, building characteristics, environmental exposure, and ownership verification — all instantly available when a loan application comes in.

A $650,000 loan on a Victorian in Portsmouth, NH. The Property Wallet shows: C2 condition, no environmental flags, clean ownership chain, recent roof and HVAC permits. The appraisal arrives — and confirms what you already knew.

Portfolio Monitoring

Refresh maintenance indicators, ownership records, and permit activity across your entire loan portfolio on a regular cadence. Properties with new permits pulled, recent deed transfers, or changes in entity ownership surface as part of the refresh — so your portfolio team works from current facts, not a stale snapshot.

The latest pipeline refresh flags three parcels in your book: one with a new 200A electrical service permit (collateral improvement), one transferred from an individual owner to an LLC last month, and one now held by an entity that controls nine other parcels. All three are facts worth knowing at your next portfolio review.

Similar Sales & Comparable Data

Every property includes pre-computed similar sales scored across 25 weighted features including condition rating, building characteristics, and permit history. Validate the appraisal’s comp selection against independently scored comparables — a C2 comp with a recent renovation permit and a C4 comp with no permits in fifteen years carry different weight, and the data explains why.

The appraisal uses three comps. You pull NE Provenance on all three: one has a recent $80K renovation permit on file and a C2 rating, another has no permits in the last decade and rates C4, the third transferred entity ownership eighteen months ago. The similar sales scoring surfaces these differences before you read the appraisal narrative.

Risk-Based Pricing & Segmentation

Segment your portfolio by property condition, environmental exposure, building characteristics, and ownership characteristics. Identify concentrations of risk that affect pricing and reserve decisions.

Of your 5,800 coastal loans across Massachusetts and Connecticut, 420 are in AE flood zones and 115 have C4-C6 condition ratings with no building permits in 10+ years. That's a segment that warrants different reserve treatment.

Permit-derived condition data with data provenance

The NEP Condition Estimate (C1–C6/NR) is derived from the permit timeline, building age, and documented renovation activity — not from imagery or on-site inspection. A C2 property has strong permit activity and multiple system updates regardless of age. An NR property has no permits on record. Every rating carries the permit timeline and methodology that supports it.

This is not a black-box score. It is a transparent, auditable estimate where every input traces to a dated municipal record. Your appraisal team can evaluate whether the permit-based estimate aligns with their on-site findings — and often it will, because documented renovation activity is the strongest available proxy for condition when imagery is not present.

NEP C1–C6/NR

Permit-activity-based condition estimate — transparent methodology, auditable inputs

FEMA NFIP

Parcel-level flood zone data for collateral risk assessment

Data Provenance

Intelligence traceable to government and proprietary sources

PDF & CSV

Export for loan files, compliance documentation, and system integration

Integration

Data that fits your systems, not just a screen

A loan officer needs a quick property lookup. Your servicing platform needs an API call at point of origination. Your portfolio team needs bulk enrichment across 20,000 loans. The same 430+ attributes are available through every delivery method.

Portfolio upload

Upload your loan tape by address. Get back condition, hazard, ownership, and environmental data on every matched property.

REST API

Per-address lookup at point of origination. Integrate property data into your LOS or servicing platform programmatically.

Batch & bulk

Up to 10,000 addresses per request. Nightly Parquet snapshots for warehouse integration. Enterprise tier.

Property Wallet

Interactive deep-dive on any individual property. Export PDF reports for the loan file with data provenance.

Your borrower data, claims history, and internal valuations stay with you. NEP adds the property data layer you can't assemble yourself — matched by address, returned alongside your existing columns.

Working together

We'll help you integrate property data into your lending workflow

Whether you're looking for a per-address API call at point of origination, bulk enrichment across your loan tape, or a pilot to evaluate our data against your current sources — we'll take the time to understand your operation and make sure the integration works.

Every conversation starts with Mike directly. We're building this for professionals who evaluate property risk for a living — and we take the partnership as seriously as you take the collateral.

Related solutions

Explore the intelligence for yourself

Open a Property Wallet for a real New England property. With over 4.7 million similar records across all six New England states, see how it fits into your workflow.

Newburyport, MA · Federalist · 3,524 sq ft · 4 bed / 3 bath · Built 1800 · Historic District

NEP Property Intelligence Summary

ConditionC1Fire ClassBFlood ZoneXOwnerIndividualOccupancyOwner-Occupied

Purchased2018 (8yr)Permits11 total · 4 in 5yrSystems3 updated · newest 0yrLiensClearAssessed$1.6MOcean0.3 miSurgeCat 2

EraPre-1940HistoricDesignatedRenovationRecent (5yr)CommercialNo Business ActivityRadonZone 1 — Highest

AES-256 encryption

US-hosted infrastructure

CCPA compliant

Customer data never sold or shared

Authoritative, primary sources

PostgreSQL — enterprise-grade infra