Solutions/Insurance

Property data for the entire carrier enterprise

NE Provenance is more than a data provider. It's an intel platform purpose-built for teams that manage carriers' core insurance functions: underwriting, actuarial & modeling, product, claims, distribution, marketing… every department that touches property risk and supports insurance operations.

The same intelligence foundation — over 1 billion data points triangulated from hundreds of sources, aerial imagery, permit-driven condition ratings, hazard exposure, risk flags and more across New England's population centers — powers different workflows across your organization. Deep regional insurance analytics and insights that drive outperformance in a market that serves over 13M individual insurance consumers.

Across your organization

One platform, every department that touches property risk

Insurance carriers are organized by department, not by data type. NE Provenance maps to how your organization actually works — the same underlying intelligence, presented for the workflow each team runs every day.

Underwriting, Actuarial & Modeling

Personal lines, commercial lines, portfolio, product, CAT underwriting, actuarial modeling, and rate development

Property data from 140+ sources for individual submissions — building characteristics, condition ratings, hazard exposure, ownership, and where available, permit history and systems age. Portfolio-level condition and risk data for territory management. Parcel-level CAT exposure for hazard underwriting. The first dataset in New England that links physical property condition to the characteristics actuaries use for rate development.

Underwriting & modeling deep divePersonal Lines Underwriting

Property-level accept/reject decisions on individual submissions — condition, construction, risk indicators, systems age

Commercial Lines Underwriting

Everything PL needs plus business classification, ISO/BOP codes, cooking operations, alcohol service, hazmat presence

Portfolio / Territory Underwriting

Condition distributions, age cohorts, permit activity rates, and risk concentrations across 5,000+ property territories

Product Underwriting

Segment profitability analysis — slice portfolios by construction type, age, condition, territory, owner type, and risk factors

CAT / Hazard Underwriting

Parcel-level flood, surge, wind, hail, and wildfire exposure — not ZIP-level aggregates

Actuarial

Property-level characteristics correlated with loss experience — construction, condition, age, territory, systems age — for rate-making and experience studies

CAT Modeling

Parcel-level exposure data by peril, geography, and construction class — enabling portfolio accumulation analysis and probable maximum loss estimation

Claims & Loss Control

Pre-loss documentation, fraud support, CAT response, subrogation, and proactive risk mitigation

Condition data, building characteristics, hazard exposure, and where available, permit history and deed records — assembled before any loss event. When a claim comes in, your adjuster sees the property picture, not a blank file. After a CAT event, triage your portfolio in the affected area by pre-existing condition.

Claims & loss control deep diveClaims Adjuster

Pre-loss condition documentation with timestamped imagery — roof, siding, foundation state before the loss event

SIU / Fraud

Compare claimed damages against documented pre-loss conditions — objective, timestamped evidence

CAT Response

Portfolio-level triage after major weather events — identify pre-existing issues vs. likely legitimate claims at scale

Subrogation

Pre-loss evidence supporting recovery efforts — construction defects, contractor records from permits, neighbor property state

Loss Control

Proactive identification of highest-risk properties — permit-gap cohorts, fire protection gaps, environmental exposure

Distribution & Marketing

Territory prospecting, lead qualification, and data-driven distribution strategy

Filter properties by owner type, condition, coverage gaps, and territory desirability — then export data-qualified prospect lists. Leads are backed by condition data, building characteristics, ownership data, and permit history where available.

Sales / Territory Manager

Data-qualified prospect lists — "1,200 owner-occupied homes across coastal Connecticut with C4+ condition, assessed over $500K, no building permit in 10 years"

Agency Manager

Territory desirability analysis — condition distributions, growth rates, and market opportunity by geography

Data delivery

Your workflow, our data, however you need it

An underwriter needs to drill into one property at point of quote. A portfolio manager needs to enrich 5,000 addresses from a book review. A CAT modeler needs bulk exposure data in their warehouse. An actuarial team needs enrichment columns joined to their own loss data. Same data — delivered the way each team works.

Portfolio Enrichment

Upload your book of business by address. We return 430+ attributes per property — condition, systems, hazard, ownership, environmental, commercial. Your data stays with you. Our data enriches it. Match by address or by owner to see the complete property picture behind every policyholder.

API & Batch Integration

Per-address REST API for point-of-quote enrichment. Batch endpoint for up to 10,000 addresses per request. Nightly Parquet snapshots with incremental deltas for warehouse integration. Our data moves in beside your existing columns — no manual lookups required.

Search & Discovery

AI-native search across 4+ million parcels. 247 filter attributes, 30+ spatial overlays, natural language queries. "Show me wood-frame coastal properties in flood zones with C4 or worse condition." Export the results or feed them into your workflow.

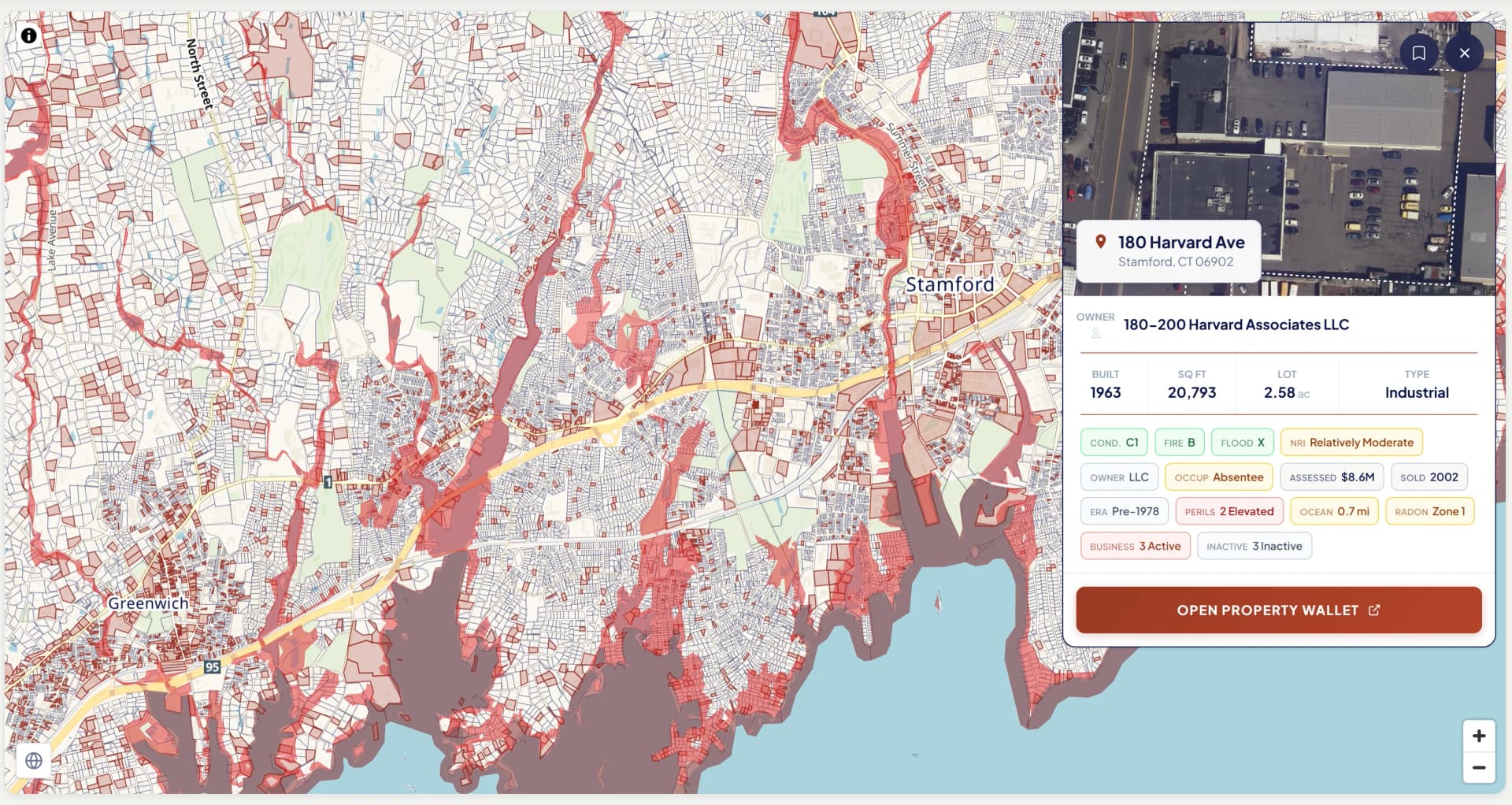

Property Wallet

Deep-dive data on any individual property — 430+ attributes across 8 tabs with built-in data provenance. The interactive exploration layer that makes the data tangible. Export individual property reports as PDF for the underwriting file.

The data behind every answer

Raw facts are evidence. Intelligence is what we sell. Over 1 billion data points from 140+ sources serve as the foundation — not the product. We triangulate across sources to answer specific questions about each property, with provenance showing what we checked, what we found, and when.

1B+

Data points

140+

Independent sources

430+

Parcel-level facts

8

Data tabs per property

Authoritative Sources

Municipal assessors, FEMA flood maps, state environmental agencies, NOAA, USDA soils, EPA, NFIRS fire incidents, registries of deeds, and county permit offices across 530+ New England communities

Derived Intelligence

Permit-derived systems age, NEP Condition Rating (C1–C6/NR), NEP Fire Protection Grade (A–E), NEP Estimated ISO class, entity detection, portfolio resolution, risk flags, and aerial imagery from all 6 state programs

Public Records Substrate

Building permits, deed transfers, mortgage recordings, lien filings, assessor updates, and ownership changes — sourced from county registries and municipal offices, refreshed as jurisdictions publish new records. Coverage varies by county and is expanding.

Standards & compliance

Built for carrier compliance from day one

Data points carry provenance — the source chain showing where data originated, who handled it, when it passed through each step. This isn't an afterthought; it's the architecture.

Our methodology aligns with state insurance bulletins on imagery-based underwriting (Massachusetts Bulletin 2025-02, Rhode Island, New Hampshire) and industry standards for property data.

COPE

Construction, Occupancy, Protection, Exposure — the four factors that define property risk

ISO

NEP Estimated ISO classification codes for commercial properties from triangulated business intelligence

NEP C1–C6/NR

Permit-activity-based condition estimate — transparent methodology, every input traces to a dated municipal record

ACORD

Export formats compatible with carrier systems and industry data exchange standards

FEMA NFIP

Flood zone designations, community ratings, and NFIP claims data integration

ASTM E2018

Property Condition Assessment standard alignment for commercial properties

Working together

We understand your operation because we've built them

17 years inside carrier operations

NE Provenance was founded by a former Senior Director and VP of Underwriting at a top-5 P&C carrier who built the workflows underwriters use every day. We know exactly what data is missing because we spent 17 years working around the gap.

We're not approaching insurance from the outside. We're rebuilding the data layer from the inside out — with the operational knowledge to make it work within existing carrier systems, compliance requirements, and decision frameworks.

We work directly with carriers to get this right

Whether you're exploring a pilot on a specific book segment, evaluating our data against what you're using today, or ready to discuss a full integration into your underwriting or claims workflow — we'll take the time to understand your operation and make sure the data fits.

Every conversation starts with Mike directly — the same person who built the pipeline and understands the carrier workflows this data serves.

Explore the intelligence for yourself

Open a Property Wallet for a real New England property. With over 4.7 million similar records across all six New England states, see how it fits into your workflow.

Newburyport, MA · Federalist · 3,524 sq ft · 4 bed / 3 bath · Built 1800 · Historic District

NEP Property Intelligence Summary

ConditionC1Fire ClassBFlood ZoneXOwnerIndividualOccupancyOwner-Occupied

Purchased2018 (8yr)Permits11 total · 4 in 5yrSystems3 updated · newest 0yrLiensClearAssessed$1.6MOcean0.3 miSurgeCat 2

EraPre-1940HistoricDesignatedRenovationRecent (5yr)CommercialNo Business ActivityRadonZone 1 — Highest

AES-256 encryption

US-hosted infrastructure

CCPA compliant

Customer data never sold or shared

Authoritative, primary sources

PostgreSQL — enterprise-grade infra