Solutions/Claims & Loss Control

The property record — dated, cited, ready at first notice

When a claim is filed, your adjuster opens a property record assembled from 140+ sources — building characteristics, condition rating, hazard exposure, environmental flags, and where available, permit history and deed transfers that document the parcel's story. Facts with dates and sources. Not opinion.

What your claims operation gets on covered New England properties

The data is assembled and dated in advance — not requested after the claim lands. Your adjuster, SIU analyst, CAT coordinator, and subrogation attorney all read from the same record.

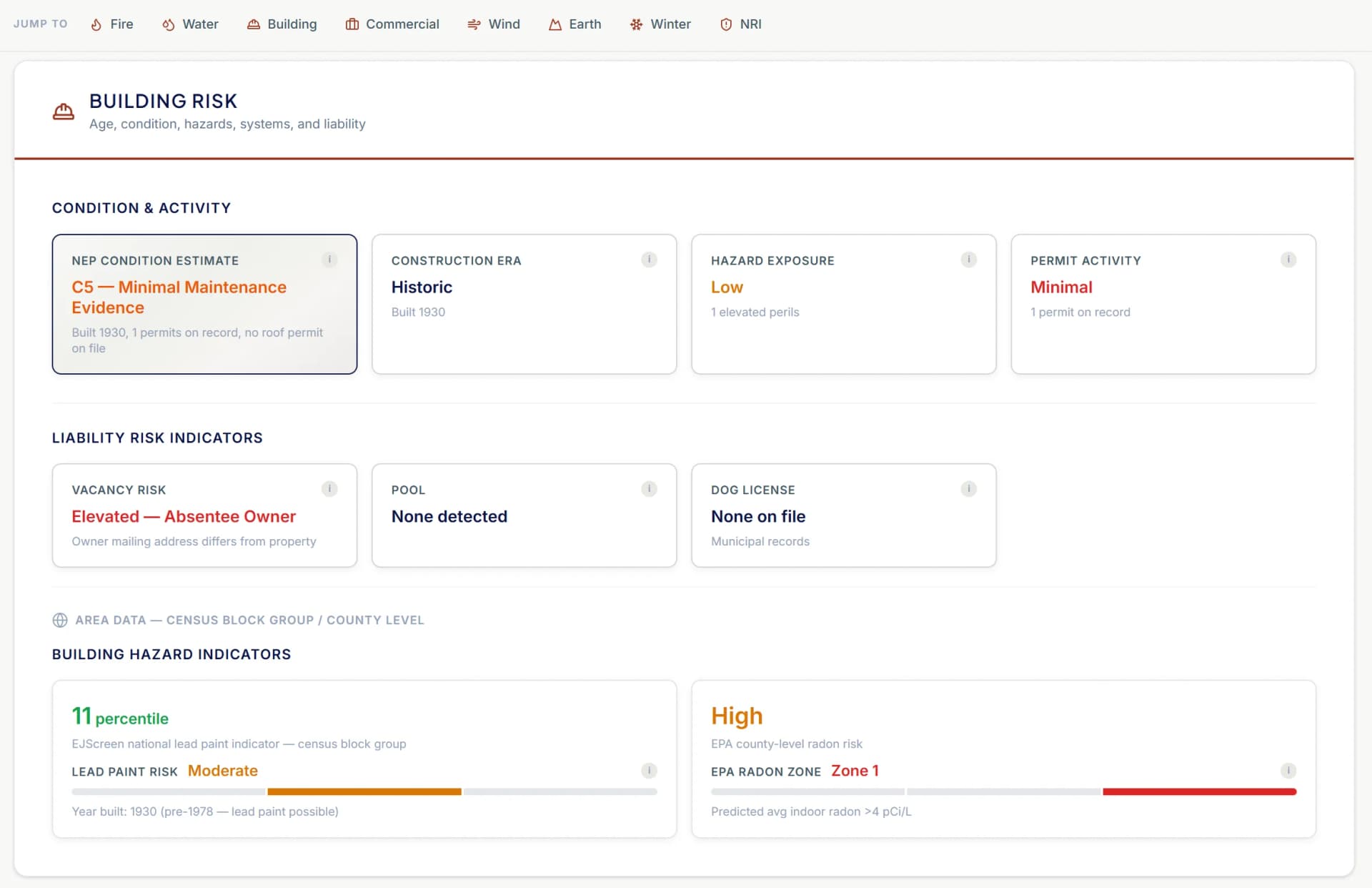

Permit timeline

Building permits on file for the parcel — date, scope of work, and contractor where listed. Roof, electrical, plumbing, HVAC, additions, and renovations from municipal permit offices across New England. Coverage varies by jurisdiction, and we’re adding communities continuously.

In practiceAt first notice of loss on a roof claim, the wallet shows the last roof permit date and scope. A 2019 tear-off on a 2024 claim is a different conversation than no roof permit on record.

Permit-derived system ages

NEP infers the age of roof, electrical, plumbing, and HVAC systems from the permit timeline. Where a permit exists, the age is dated. Where no permit exists, the field is marked indeterminate — we do not guess.

In practiceWater damage claim on a property with a 2022 plumbing repipe permit reads differently than one with no plumbing permit since the 1978 build date.

Ownership chain and entity type

Deed transfers on the parcel with date, price, grantor, and grantee — sourced from county registries of deeds across New England. Entity resolution identifies LLC, trust, and corporate owners. Ownership duration and recent transfers are facts — the interpretation belongs to your team.

In practiceA property that transferred 90 days before a claim event, or is held by an LLC that owns eight other parcels, is context the adjuster should have going in.

Hazard and environmental bundle

FEMA flood zone, NOAA hurricane surge category, NRI composite, wildfire exposure, wind, hail, earthquake, dam inundation (elevation-aware), and environmental flags — 21E sites, AULs, USTs, wetlands, radon zone. Parcel-level, not ZIP-aggregated.

In practiceAfter a coastal storm event, filter the affected area by flood zone, surge category, and the year of the most recent roofing permit. Triage the portfolio, not one property at a time.

NEP Condition Rating (C1–C6 / NR)

A condition estimate derived from the permit timeline, building age, and structural characteristics. Properties with no permit history at all are rated NR (No Record) rather than being penalized — inconclusive is better than wrong. Methodology is documented and cited on every property.

In practiceA portfolio view showing the distribution of C1–C6 and NR across an affected CAT zone lets the claims leader allocate adjusters by likely severity.

Fire Protection Grade

An A–E grade scoring two factors: distance to the nearest responding fire station (from HIFLD national fire station data) and whether the parcel has municipal water/sewer service. A property close to a station with municipal water scores higher than one on well/septic at the same distance. Every parcel in the coverage area has a grade.

In practiceA Grade E property (station over 3 miles, no municipal water) is a fundamentally different response-time and suppression expectation than a Grade A property with a station under a mile and municipal service.

How claims teams use it

The same property record serves four distinct claims workflows. The data is the same; the questions the data answers are different.

First notice and adjusting

The adjuster opens the claim with the property record already in hand. Building characteristics, permit timeline, system ages, ownership, hazard exposure, and condition rating — dated and cited. The file is no longer empty at intake.

SIU and fraud review

Permit records, deed transfers, and condition ratings provide objective, timestamped facts. If the claim narrative is inconsistent with what’s documented — for example, a claim of recent renovation with no building permit on file — that is a fact-based question SIU can raise and investigate.

CAT response and triage

After a declared event, filter the affected geography by flood zone, surge category, wind exposure, building age, and condition rating. Prioritize adjuster deployment against the portfolio segments most likely to carry real severity. Portfolio visibility in minutes.

Subrogation and recovery

Permit records identify the contractor of record and the scope of work for any permitted renovation. Where a construction defect contributes to loss, the permit file points recovery counsel at the right parties. The parcel-level hazard bundle supports claims against common-enemy and governmental parties where applicable.

Loss control and risk mitigation

Proactively identify the highest-risk properties in your book before losses occur. Filter by permit-gap cohorts, fire protection grade, condition rating, environmental exposure, and building age to surface properties that warrant inspection, mitigation recommendations, or underwriting action. The same data that supports claims after a loss supports loss control before one.

Delivery for claims teams

Property data at first notice — not after a week of research

Claims teams need the property record immediately when a loss is reported, and at portfolio scale when a CAT event hits. The data is available however your systems need to consume it.

API at FNOL

Per-address lookup returns the full property record at first notice of loss. Integrate into your claims management system so adjusters see the property picture before making the first call.

Batch for CAT triage

Upload the affected portfolio after a major weather event. Get back condition baselines, hazard exposure, and permit history for every property in the impact zone — triage at portfolio scale in minutes.

PDF for the file

Export a dated, source-attributed Property Wallet report for the claims file. Pre-loss documentation with provenance that supports adjusting, SIU, and subrogation workflows.

What this record is, and what it is not

NE Provenance gives your claims team a dated, cited property history assembled from authoritative public sources. It is a factual substrate your adjusters, SIU team, and CAT coordinators can build on. It is not a replacement for on-site inspection, forensic engineering, or the human judgment your claims organization brings to every file.

We do not predict fraud. We do not assign intent to homeowners. We do not correlate personal circumstances with property condition. The data is structural: what the building is, what has been done to it, who has owned it, what hazards surround it, and how that picture compares against the rest of the book. What to do with that picture is your team's call.

Our first principle is that inconclusive is better than wrong. Where we have a fact, we cite it. Where we do not, we say so. The property record is only as trustworthy as the sources behind each value — which is why every value in the wallet carries its source attribution.

Explore the intelligence for yourself

Open a Property Wallet for a real New England property. With over 4.7 million similar records across all six New England states, see how it fits into your workflow.

Newburyport, MA · Federalist · 3,524 sq ft · 4 bed / 3 bath · Built 1800 · Historic District

NEP Property Intelligence Summary

ConditionC1Fire ClassBFlood ZoneXOwnerIndividualOccupancyOwner-Occupied

Purchased2018 (8yr)Permits11 total · 4 in 5yrSystems3 updated · newest 0yrLiensClearAssessed$1.6MOcean0.3 miSurgeCat 2

EraPre-1940HistoricDesignatedRenovationRecent (5yr)CommercialNo Business ActivityRadonZone 1 — Highest

AES-256 encryption

US-hosted infrastructure

CCPA compliant

Customer data never sold or shared

Authoritative, primary sources

PostgreSQL — enterprise-grade infra